How Do Financial Advisors Keep Clients After Death, Divorce, or Incapacity?

How Do Financial Advisors Keep Clients After Death, Divorce, or Incapacity?

(Death, Divorce, Incapacity—and Why Most Advisors Lose the Relationship Anyway)

By Vance Morris

Most financial advisors think they lose clients because of performance, fees, or bad advice. They lose them when life shows up uninvited.

Death.

Divorce.

Incapacity.

That’s when everything gets tested. Not your portfolio… your relationship. And in my experience, most advisors fail that test.

Why Understanding These Moments Actually Matters

These aren’t edge cases, but inevitabilities. And how they’re handled determines whether:

assets stay

relationships survive

or everything walks out the door to a new advisor who just happened to show up at the right time

You can be technically perfect…

…and still lose the client.

This isn’t about your technical skill, but about how trust moves or doesn’t.

How Relationship “Transfer” Actually Works

When life changes, control shifts. Not emotionally. Legally. And the system doesn’t care how great your quarterly reviews were. Custodians follow:

account titles

beneficiary designations

legal documents

Not loyalty. Not history. Not how long you’ve “worked together.” If trust isn’t already embedded beyond you…

…it doesn’t transfer.

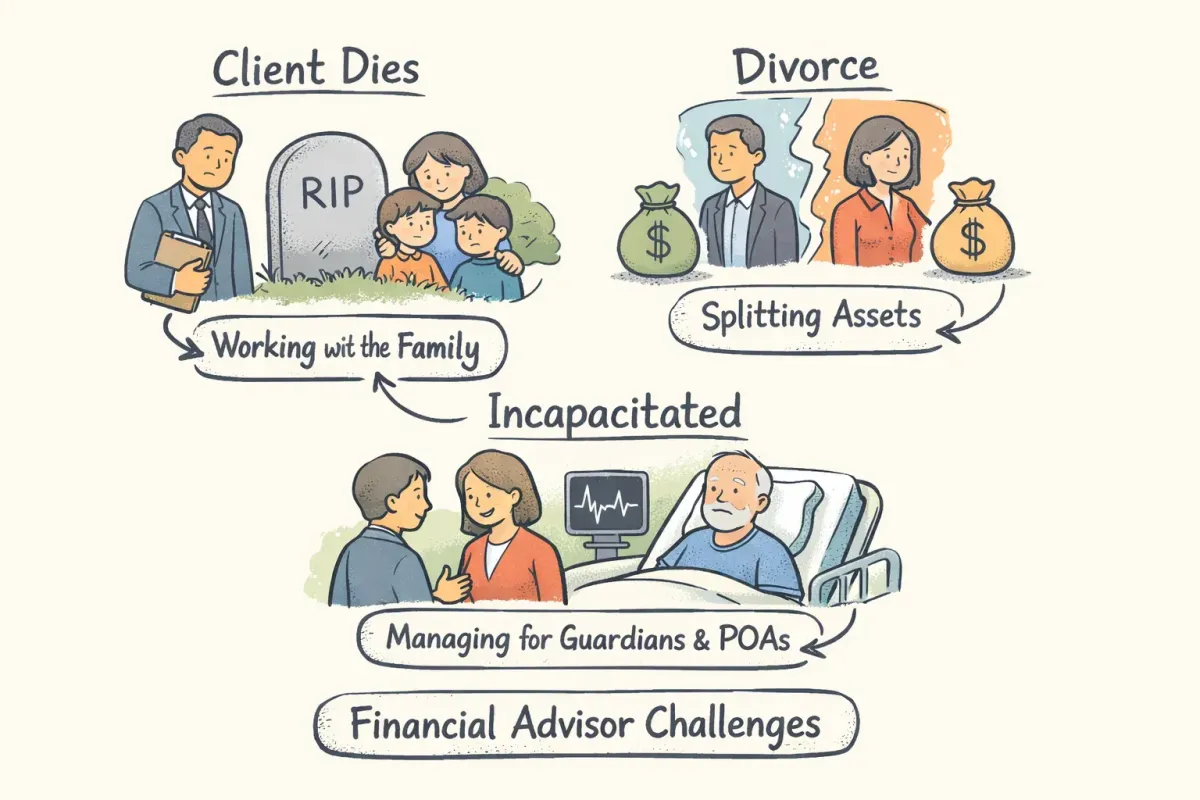

What Happens When a Client Dies

(Heirs, Executors, and the Reality Check)

When a client dies, the custodian doesn’t ask, “Who had the best relationship?” They look at paperwork.

Beneficiary designations override wills

Joint accounts pass automatically

Everything else goes through probate

To move anything, custodians typically require:

certified death certificate

letters testamentary or trustee certification

ID for the new owner

account transfer forms

Until that’s verified? Trading usually stops, access slows down and your “relationship” is now sitting in limbo while the family decides what to do next. You can assist:

inventory holdings

identify tax lots

coordinate with estate counsel

But here’s the real question:

👉 Does the family even see you as their advisor?

Because if they don’t, you’re just a temporary placeholder. Processing can take days… or weeks. Want to speed it up? Have:

certified documents ready

executor or trustee clearly identified

estate counsel looped in early

That’s operations. But retention? That was decided long before the death.

When Divorce Hits

(Splitting Assets—and Usually the Relationship Too)

Divorce doesn’t just split assets, it splits trust. Ownership changes based on state law:

Community property → roughly 50/50

Equitable division → based on circumstances

Retirement accounts often require a 👉 qualified domestic relations order (QDRO) to avoid tax disasters.

Here’s where advisors get into trouble. When both spouses are clients, things get messy, fast.

You’ve got:

conflicting interests

emotional landmines

legal exposure

Smart move?

disclose conflicts immediately

pause joint planning when needed

recommend independent counsel

Put it in writing:

who you represent

when services stop

when separation is required

After the dust settles:

confirm new account titles

clarify fees

define who continues with you

But let’s not pretend. Most of the time? You don’t “retain both.” You’re lucky if you retain one.

When a Client Becomes Incapacitated

(Who Actually Has Control?)

Now we’re in dangerous territory. Because if nobody planned for this… everything slows to a crawl.

Two main paths:

Durable Power of Attorney (POA)

Named agent acts immediately

No court involvement

Guardianship / Conservatorship

Court-appointed

Slow, expensive, messy

Custodians typically want:

original or certified POA

proper notarization

sometimes additional institutional verification

Before you move a dollar:

confirm it’s durable

check for revocation

verify with the drafting attorney if needed

Also:

require ID from the agent

watch for unusual activity

question anything that smells off

If something feels wrong? Stop. Refuse instructions and report it if necessary.

Because at this stage, you’re not just an advisor, you’re a gatekeeper.

What Actually Determines If the Relationship Survives

Let’s cut through it.

It’s not:

performance

reporting

your charming personality

It’s whether the relationship was built to survive you.

The Three Types of Advisor Relationships

Performance-Based

Built on returns

Looks strong

Collapses under stress

Service-Based

Responsive, helpful

Better… but still fragile

Experience-Based

Multi-person trust

Emotional connection

Survives life events

Most advisors live in the first two. The third is where retention actually happens.

The Variables That Decide the Outcome

Just like brewing coffee, small variables change everything.

Here, it’s:

involvement of spouse and heirs

frequency of meaningful communication

clarity of roles during transitions

documented continuity plans

proactive touchpoints before life events

Ignore these…

and you’re gambling with your book.

The Myths That Are Costing Advisors Millions

Let’s clear this up.

“Great performance keeps clients.” No. It keeps them… until something happens.

“Good service builds loyalty.” No. It builds satisfaction, not attachment.

“Clients are loyal.” No. They’re loyal to certainty, clarity, and comfort.

Lose those? They’re gone.

Choosing an Advisor Who Can Actually Handle This

If you’re evaluating an advisor, or positioning yourself as one, this is where it matters.

Credentials help:

CFP® → broad planning expertise

RIA → fiduciary obligation

Groups like NAPFA often signal fee-only models, but verify everything.

Fee structure matters more than people admit:

AUM can drop when assets split

Flat or hourly is easier to carry across transitions

Commissions can complicate everything

If you want a breakdown of how advisors actually price their services,

see this analysis.

Continuity is the real differentiator.

Ask:

Is there a written succession plan?

Who is the backup advisor?

Have they met the spouse or heirs?

Or is everything sitting in one person’s head?

For a deeper look at operationalizing this, see Vance Morris | Architect of XPerience Service Systems for Wealth Advisors.

The Vetting Checklist (Use This or Pay Later)

Ask directly:

“Are you a fiduciary 100% of the time?” Get it in writing.

For a plain-English breakdown, see what is the fiduciary duty.

“What happens if you disappear tomorrow?”

There better be a name, a process, and an introduction.

“Can I see your continuity plan?”

If they hesitate… that’s your answer.

Red Flags That Should Make You Walk

No succession plan

Vague fiduciary answers

Heavy reliance on commissions

Too many clients, not enough structure

Refusal to include spouse or heirs

Quick scoring:

Must-haves:

Written fiduciary status

Documented succession plan

Spouse/heir inclusion

Extras:

Backup advisors

Team structure

Fee transparency

Client references

Miss the must-haves?

Move on.

Where to Find Better Advisors

Start with:

CFP Board

NAPFA

XY Planning Network

Paladin Registry

RIA firms with published fees

For curated fee-only options, see the Flat Fee Advisors directory.

The 72-Hour Reality Checklist (After Life Hits)

When something happens, speed matters.

Within 72 hours:

notify advisor and custodian

secure death certificates

gather wills and trust docs

confirm executor or trustee

freeze unnecessary transfers

schedule a planning call within 10 business days

Bring:

account numbers

beneficiary forms

POA or trust documents

Delays cost money and confusion costs relationships.

What This Means for Your Practice

Death, divorce, and incapacity don’t just change accounts.

They change control.

Beneficiaries dictate flow

State law dictates splits

POAs or courts dictate authority

If this isn’t documented and systemized…

your team will hesitate.

And hesitation is where assets leak.

For deeper guidance on retirement splits, see qualified domestic relations orders (QDROs).

Where Most Advisors Lose the Game

Not in the markets.

In the moments that matter.

when heirs don’t know them

when spouses aren’t included

when no one knows what happens next

That’s when relationships fracture and when accounts move.

If you want a wake-up call, read Why Your Clients Feel Replaceable 02.19.26

And if you think authority is guaranteed in today’s world… it’s not. See "Botox" Killing Your Financial Advisory Authority.

The Move Most Advisors Avoid (And Pay For Later)

Audit your top ten clients right now.

Are beneficiaries current?

Is there a durable POA?

Has the spouse met you?

Do heirs know your name?

If not…

you don’t have a client relationship, but a temporary arrangement.

Legal authority decides who controls the account. But experience… systems… and communication?

That’s what decides whether you’re still in the picture when it matters.